Geopolitical shockwaves strike food and drink packaging

Food and drink manufacturers already battling tight margins just got hit with a volatile second quarter in 2026.

Data from the Flexible Packaging Europe (FPE) Raw Material Price Index confirms that geopolitical tensions — chiefly driven by the recent Iran crisis and disruptions around the Strait of Hormuz — have triggered an unprecedented price spike across every major packaging substrate.

For a trade heavily dependent on plastics, foils, and papers to keep products shelf-stable, these soaring overheads are accelerating fears of heightened food inflation and diminished consumer spending.

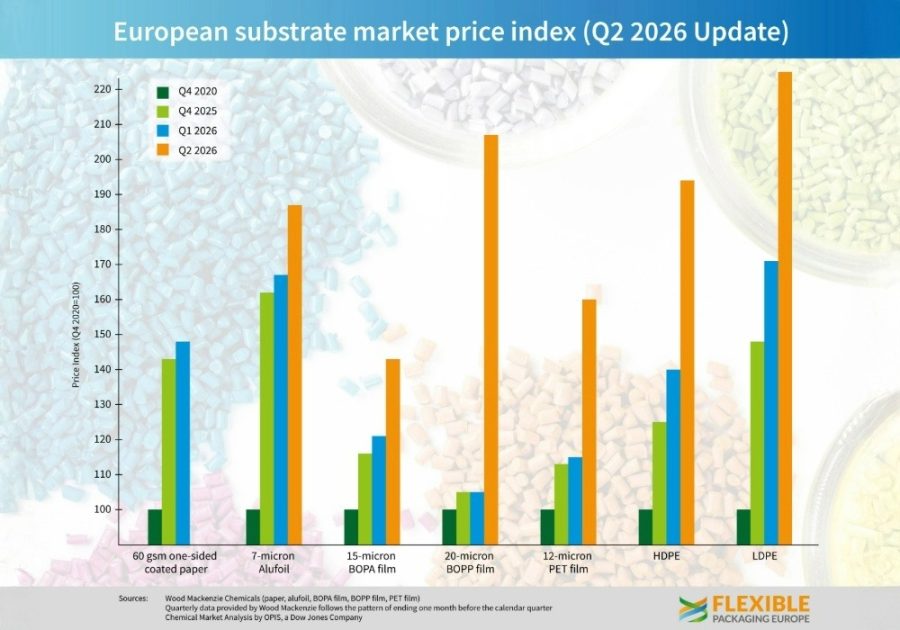

The Q2 2026 Price Surge

The second quarter saw rapid cost escalation across all flexible substrates compared to Q1, caught between low initial European inventories and sudden supply-chain bottlenecks.

| Material substrate | Q2 price increase vs. Q1 | Primary driver |

| BOPP film (20 micron) | +97% | Severe European polypropylene resin shortages |

| PET film (12 micron) | +40% (+€0.55/kg) | Rising oil prices; acute PTA and MEG shortages |

| HDPE | +38% | Volatility from Middle East supply displacement |

| LDPE | +31% | Panic buying prioritising availability over cost |

| BOPA film (15 micron) | +21% | Escalating costs of PA6, PA66, and caprolactam |

| Aluminium foil (7 micron) | +12% (+€0.62/kg) | Higher LME prices and massive warehouse premiums |

| One-side coated paper (60 gsm) | <5% (+€0.06/kg) | Lagging pressure from sustained winter energy costs |

Anatomy of a supply shock

The sharp market shift in March through May highlights just how fragile European packaging lines are to global energy and trade flows. When the Iran crisis threatened a massive supply disruption, buyers abandoned cost negotiations and pivoted entirely to securing material availability.

This panic buying collided with naturally low European resin inventories. Middle Eastern production flows were displaced, and alternative international suppliers struggled to reconfigure shipping lanes fast enough to fill the gap. Consequently, prices for standard polymers like polyethylene (HDPE and LDPE) shot up dramatically within a matter of weeks.

Even less oil-dependent materials felt the squeeze. Aluminum foil surged due to London Metal Exchange (LME) spikes and soaring warehouse premiums, while paper processing braced for the delayed economic impact of sustained high energy prices.

What This Means for the Grocery Aisle

While European flexible packaging suppliers successfully delivered all requested volumes without systemic line stoppages, the financial damage is already rippling down the supply chain.

Food and drink processors cannot absorb double-digit increases in core packaging materials indefinitely. Industry bodies, including the Food and Drink Federation (FDF), have already raised their late-2026 food inflation forecasts to 9% or higher to account for these rising fossil fuel, transport, and packaging inputs. The ultimate concern for brands is no longer material availability, but “shelf shock” — the risk that upcoming retail price hikes will severely dampen general private consumption.

The H2 outlook: is the peak behind us?

Data from late June suggests the worst of the sudden price spike has plateaued. As buyers shifted their focus from hoarding material to affordability, more competitive offers from international markets — particularly China — helped spot prices ease.

The prospect of a potential diplomatic agreement between the United States and Iran, alongside the gradual reopening of the Strait of Hormuz, is already weighing down crude oil and feedstock baselines. If these supply chain bottlenecks continue to dissolve, polymer and packaging prices should normalise through the second half of 2026. However, because spot prices remain well above pre-crisis levels, food and beverage procurement teams must prepare for elevated packaging overheads to persist well into autumn.